Inflation expectations and Treasury yields inch higher

January 12, 2018 | 2 minute read

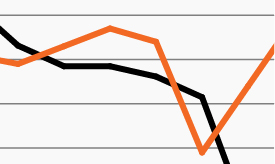

Inflation expectations have slowly edged up in recent weeks, after reaching a low in June 2017. As the chart highlights, for example, the 5-year Breakeven Inflation Rate, which represents expected inflation over the 5-year period, has risen approximately 5 bps year to date and has nearly reached the 2% mark.1 Longer-term inflation expectations have remained just above 2% since the start of 2018.1

Price expectations moved higher primarily on account of firming oil prices, which reached a three-year high this week, but also with continued solid economic data across the developed world and optimism surrounding the recently signed U.S. tax plan.2

The yield on the 10-year Treasury note has risen for many of the same reasons as inflation expectations. This week, it neared the upper end of the 2.2%–2.6% band inside which it has traded since early 2017.3

Even taking recent upward trends into account, however, each measure remains well in check when looking at them over a longer time period.

Inflation expectations moved briefly above 2% in early 2017, but dipped back down through the remainder of the year and remain well below their post-crisis average.1 Likewise, the 10-year Treasury note remains within its recent cyclical trading range.3 Even after the Fed’s five rate hikes this cycle, however, the measure is comfortably under its post-crisis high.