At its first meeting of 2018, the Fed stays the course

This Fed rate hike cycle remains on a slow and shallow trajectory

February 2, 2018 | 2 minute read

In recent weeks, investors have increasingly focused on the potential for accelerated economic growth to stoke inflationary pressures within the U.S. economy. January’s strong wage growth provided evidence that rising prices could indeed be a challenge on the horizon for investors.1 Yet PCE data showed no sign of inflationary pressures percolating within the U.S. economy. In fact, on a year-over-year basis, the PCE Index declined in December from one month earlier.2

Within this context, the FOMC at its first meeting of 2018 maintained the target federal funds rate at 1.25%–1.5%.3 The meeting was Janet Yellen’s final as Fed Chair and was perhaps a fitting end to Ms. Yellen’s tenure, which has been marked by a slow and steady approach to raising rates throughout the economic recovery.

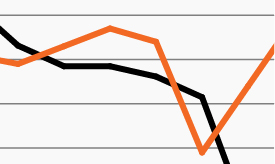

In the current cycle, for example, the FOMC has raised the target federal funds rate five times for a total of 125 bps since it began tightening more than two years ago.4 If current projections hold true under the leadership of new Chair Jerome Powell, the target federal funds rate will rise another approximately 140 bps from now until 2021.5

As the chart highlights, the current tightening path has been significantly slower and shallower than for any other hiking cycles since 1986.4 In that timeframe, the FOMC has engaged in five sustained rate hike cycles. The cycles have ranged from as little as a 150 bps hike over a 12-month period (starting in June 1999) to as much as the 425 bps increase that began in June 2004 and lasted for two years.4

However, as recent economic growth estimates firm and average hourly wage data jumps, policymakers may face a significant test in 2018 as they seek to balance what has been their cautious approach toward raising rates with the potential for more robust economic growth and higher inflation expectations ahead.1,6