Fed comments point to a slow rate-hike trajectory despite strong headline wage growth

Average hourly earnings rose the most for managers in January

February 9, 2018 | 1 minute read

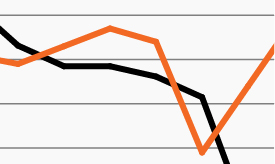

Last Friday’s jobs report brought to the forefront long-dormant fears that inflationary pressures may finally be emerging, as average hourly earnings for all private sector employees rose at their highest annual rate since June 2009.1

Parsing the strong headline number, however, one can see that the wage increases were not evenly distributed across all workers. For example, wages for nonsupervisory employees, who account for approximately 82% of all employment in the U.S., remained flat in January at just 2.4% annual growth.2,3 Further, January’s nonsupervisory employees’ wages were relatively in line with the 2.3% average wage growth they saw in 2017.3

As some investors fret about the Fed accelerating its activity, policymakers appear confident that they will remain on a slow trajectory in raising rates.

John Williams, President of the Federal Reserve Bank of San Francisco, reiterated in a speech just last week that the FOMC won’t overreact in the months ahead. Williams noted that his message to those “concerned about a knee-jerk reaction from the Fed is that, as always, we’ll keep our focus on the dual mandate and let the data guide our decisions.”4