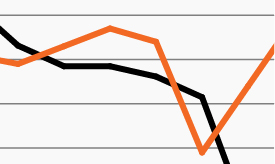

Sluggish productivity growth has helped keep interest rates in check

Productivity growth and interest rates remain below their long-term averages

March 9, 2018 | 2 minute read

Market expectations for four rate hikes in 2018 continued to climb this week, despite ongoing volatility in the U.S. credit and equity markets. The market-implied probability that the Federal Reserve will raise the target federal funds rate four times this year reached approximately 35% this week, up from approximately 12% at the beginning of this year.1

For their part, members of the FOMC have not discouraged such expectations in recent appearances. Fed Governor Lael Brainard this week noted the strong headwinds that “weighed down the path of policy” several years ago and acknowledged “the reverse could hold true” today.2 Brainard’s comments echoed those of Fed Chair Jerome Powell one week earlier.3

As investors weigh policymakers’ recent hawkish comments with the generally improving economic environment, however, it is important to keep in mind that long-term natural interest rates today could remain well below those of the past several decades.

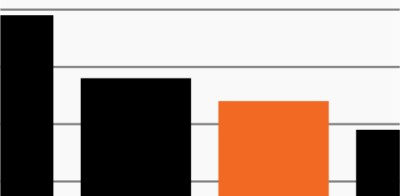

In its December 2017 Summary of Economic Projections, for example, the FOMC estimated the longer-run federal funds rate to reach just 2.8%, only approximately 1.4% above where it stands today and well below its average of approximately 5.5% during the last three economic expansions.4,5

Additionally, data released this week showed that nonfarm productivity growth was flat in the fourth quarter of 2017 and underscored the potential constraints that policymakers may face in the years ahead.6 Worker productivity is a key driver to economic growth and, absent significant improvements, investors could remain in economic and market environments defined by sluggish growth and relatively low interest rates in the coming years.

Advisors expect to reduce their clients’ cash allocations this year. Alternatives, multi-asset and real asset investments are among the major beneficiaries.