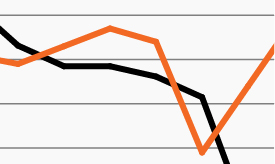

U.S. Treasury yield curve flattens again as inflation data moderates

Spread between 10-year and 2-year Treasury notes

March 16, 2018 | 1 minute read

Bond investors have tightened their focus on inflation data in recent months, particularly after January’s nonfarm payrolls report suggested U.S. wages were finally beginning to rise.1 Then, January’s stronger-than-expected rise in core CPI prices appeared to confirm the trend of rising prices.2

One result was a notable jump in U.S. Treasury yields during the first two months of 2018. By the third week of February, the U.S. 10-year Treasury yield had risen to a four-year high of 2.94%, and the U.S. 30-year Treasury yield was sitting above 3.20% for the first time since 2015.3,4

Since then, investor concerns have eased noticeably as recent data suggests inflation pressures remain muted. This week’s CPI report showed headline prices rising only modestly and core prices remaining flat.2 And while February’s nonfarm payrolls report showed a jump in jobs growth, it also showed average hourly earnings growth slowing from January’s pace.1

This week, long-end U.S. Treasury yields declined again after U.S. retail sales fell 0.1% in February, further suggesting that U.S. economic growth and inflation remain subdued despite a tightening labor market and rising consumer confidence.5

This has translated into a flatter U.S. Treasury yield curve in March than last month. After steepening sharply in early February, the spread between the 10-year and 2-year Treasury yields has declined by approximately 20 basis points as investors, once again, appear to be dialing back their long-run inflation expectations.6

With inflation in check, the U.S. Federal Reserve is more likely to remain on its current pace of gradual interest rate increases.