See why increased volatility and minimal returns across domestic and global markets could continue through the year end.

October 26, 2018 | 1 minute read

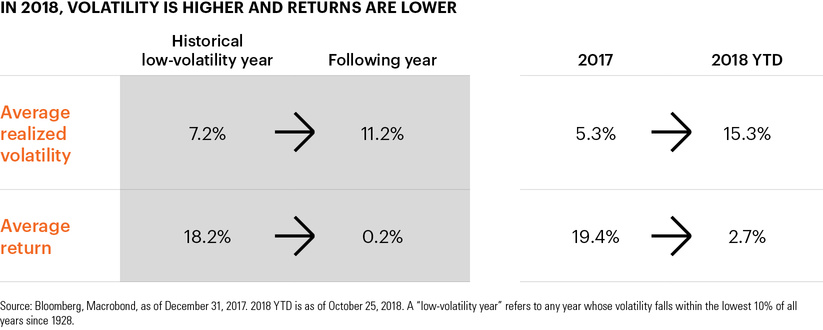

Market performance in October highlights a larger trend that investors have been seeing throughout 2018. Specifically, traditional equity market indexes have generated relatively low returns YTD while volatility has increased compared to 2017.

As we noted in June, this has historically occurred the year following a “low-volatility year.”1 After returning nearly 20% last year, the S&P 500 Index has returned just 2.7% YTD. Meanwhile, realized volatility has nearly tripled, from just 5.3% in 2017 to 15.3% in 2018.2

Notably, investors have not been able to turn to other major markets to generate higher returns. Small-cap U.S. stocks have declined 1.3% while international stocks have fallen more than 10%.3

Traditional fixed income markets have also faced challenges this year. The Bloomberg Barclays U.S. Aggregate Bond Index is down over 2% year to date as traditional safe-haven investments, such as Treasuries and investment grade corporate bonds, have underperformed shorter-duration investments.

Recent volatility has been driven by investors focused on the possibility that global economic growth could dampen in 2019, corporate earnings growth may soften or geopolitical concerns could become further aggravated.

Against this backdrop, investors may be well served preparing for the potential for a more muted return environment compared to recent years, coupled with periods of heightened volatility.

This week’s chart looks at return drivers for middle market buyout transactions, which have generated higher realized capital multiples than large cap and may favor middle market managers looking forward.