As rate concerns fade, so does investor interest in loans

See how investor interest in high yield bonds and senior secured loans has shifted in what’s now a firmly accommodative environment.

March 29, 2019 | 2 minute read

The 10-year U.S. Treasury yield reached a 15-month low this week and has declined nearly 40 bps since March 1.1 The decline has come as the Fed affirmed that it will remain on the sidelines for now and amid a fresh bout of soft economic releases in the U.S. and EU.

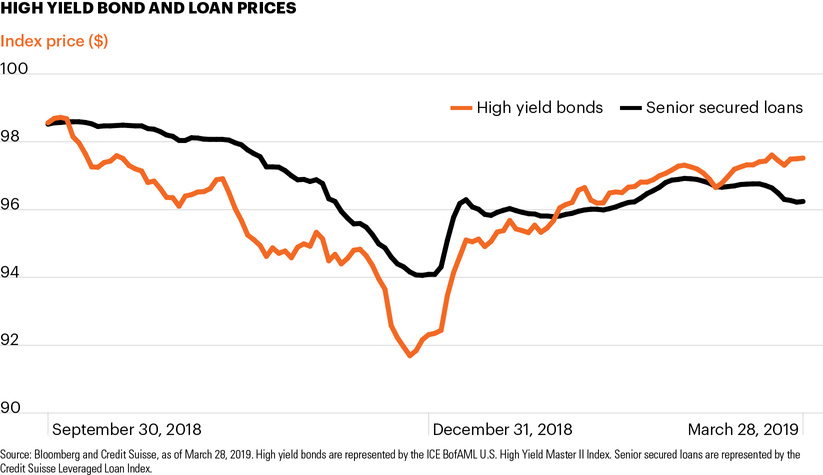

Within a now firmly accommodative environment, high yield bonds and senior secured loans have moved off their late-December lows, but have not fully recovered from the decline experienced in Q4 2018.2

Against this backdrop, high yield bond funds have seen YTD inflows of $12.3 billion versus the historic outflows they experienced in Q4 2018.3 High yield bonds have benefited this year as the U.S. economy continues to experience slow-but-positive growth with minimal inflation pressures and as the Fed’s shift has further compressed yields across traditional fixed income asset classes.

On the other hand, as rate fears have diminished, investors have exited low-duration floating rate assets. Investors withdrew nearly $1.4 billion from bank loan mutual funds during the week ended March 27 and have withdrawn approximately $9.5 billion YTD.3

Shifting investor sentiment over the last six months serves as a timely reminder of how market technicals (supply/demand), rather than fundamentals, can drive credit prices. The decline in credit prices occurred in the fourth quarter against the backdrop of generally strong corporate fundamentals marked by low defaults. High yield bond and senior secured loan defaults ended 2018 at 1.8% and 1.6% respectively.4

These periods may create opportunities for managers with the expertise and liquidity to take advantage of investments arising from the volatility and shifting investor sentiment.