See how dipping inflation expectations support a Fed rate cut, which would signal further troubles for income-oriented investors.

June 14, 2019 | 1 minute read

The usual categorizing of policymakers along a spectrum from hawkish to dovish has evolved recently into a conversation about those willing to remain patient with the current policy rate vs. those ready to cut interest rates soon. Data released this week may provide another reason to push policymakers into the rate-cutting camp.

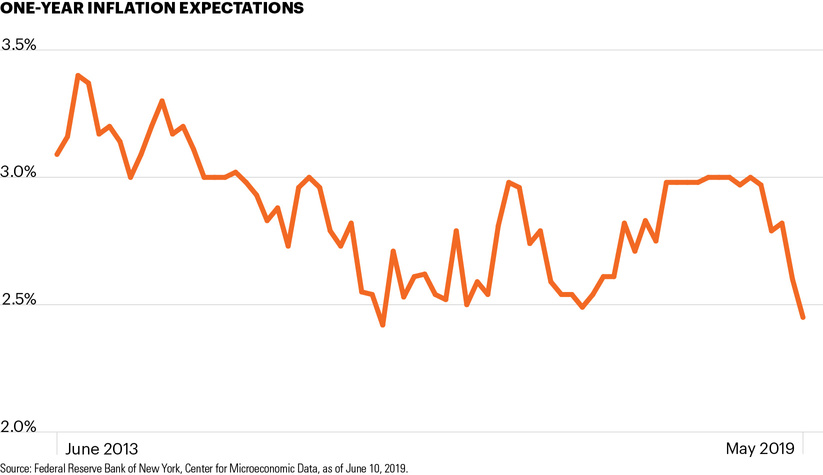

On Monday, the New York Fed reported in its May 2019 Survey of Consumer Expectations that median inflation expectations declined another 15 bps over a one-year horizon and 10 bps over three years. One-year inflation expectations fell to their lowest reading since January 2017.1

Consumer price index (CPI) data, also released this week, showed that inflation pressures have slowed for each of the past three months. CPI increased at a rate of just 0.1% in May and 1.8% on an annual basis.2

By nearly all measures, inflation has been running under 2% since the Fed set it as a target in 2012. Sentiment data like the New York Fed released this week is especially important, however, because research shows that expectations have become “the dominant factor” in explaining inflation dynamics since the Great Recession.3

The market currently assigns an 85% probability that the Fed will lower rates at its July meeting.4 Markets will likely be disappointed if the Fed doesn’t signal a lower direction at its June meeting. However, sending that signal would confirm for income-oriented investors there’s no end in sight to the current era of low interest rates.