Rates are set to remain lower for even longer after Fed cut

See why the Fed’s third interest rate cut this year and market expectations of a fourth by the end of 2020 create a bleak outlook for yield-hungry investors.

November 1, 2019 | 2 minute read

As expected, the FOMC cut interest rates at its meeting this week, citing weak global growth prospects and muted inflation pressures. The Fed has now cut interest rates three times since July, quickly reversing 75 bps of the 2.25% in rate hikes it had enacted in the earlier hiking cycle.

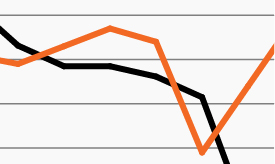

Even after this week’s rate cut, investors expect at least another cut by the end of next year. As the chart shows, investor expectations for the target Fed funds rate in December 2020 have gradually declined over the last year.1 In fact, markets are pricing in an additional 35 bps reduction between now and December 2020.1

The Fed’s accommodative approach has helped boost year-to-date returns of stocks (S&P 500 +23.3%) and bonds (Barclays Agg +8.9%).1

However, looking more closely at what has driven fixed income returns this year reveals a bleak outlook for yield-hungry investors. The vast majority of the Barclays Agg’s return has come from price appreciation thanks in large part to the latest round of Fed cuts.1 Meanwhile, income has represented an increasingly small fraction of the Barclays Agg’s total return since the 1990s and accounts for approximately just 2% of its nearly 9% YTD total return.1

With interest rates already near historic lows, fixed income investors may not be able to rely on falling rates to drive returns. Increasingly, investors may need to turn to alternative sources of income as the current lower-for-longer environment does not appear ready to recede anytime soon.