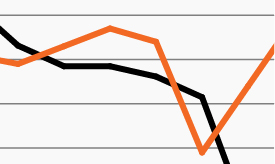

A quick roundtrip: yields return to pre-COVID levels

Back to low or no yield? Our chart looks at why fixed income investors need to look outside of traditional markets for competitive opportunities.

June 19, 2020 | 1 minute read

Quick action by the Federal Reserve helped spark equity and fixed income markets’ robust rebound in late March as the Fed brought rates back to the zero lower bound, initiated unlimited quantitative easing and employed a host of other liquidity measures to help stabilize markets.

As the market rally carried into Q2 through early June, U.S. investment grade corporate bonds rose as much 8.0% while high yield bonds returned approximately 12.5%. Both asset classes retraced some of their gains through the balance of June.1

The Fed once again helped kickstart a rally this week (in conjunction with a strong bounce in retail sales data), announcing it will begin buying individual corporate bonds in addition to the bond ETF purchases previously implemented under its Secondary Market Corporate Credit Facility.

Major fixed income markets reacted quickly to the news, with yields on the Barclays Agg and the 10-year U.S. Treasury plunging approximately -8% and -16%, respectively, lower than where they began June.2 (A bond’s yield and price move in opposite directions.)

While investors can certainly cheer the market’s strong rebound since late March, income-oriented investors now find themselves almost exactly where they were prior to the pandemic – in a low- to no-yield world.