Spike in HY issuance stresses the importance of active management

Sales surging after near collapse? Our chart looks at how the massive spike in new high yield issues displays the importance of active management.

June 26, 2020 | 2 minute read

Since bottoming in late February, the high yield bond market has recovered almost as quickly as it declined. The asset class has benefited from unprecedented monetary and fiscal stimulus along with optimism surrounding a reopening U.S. economy.

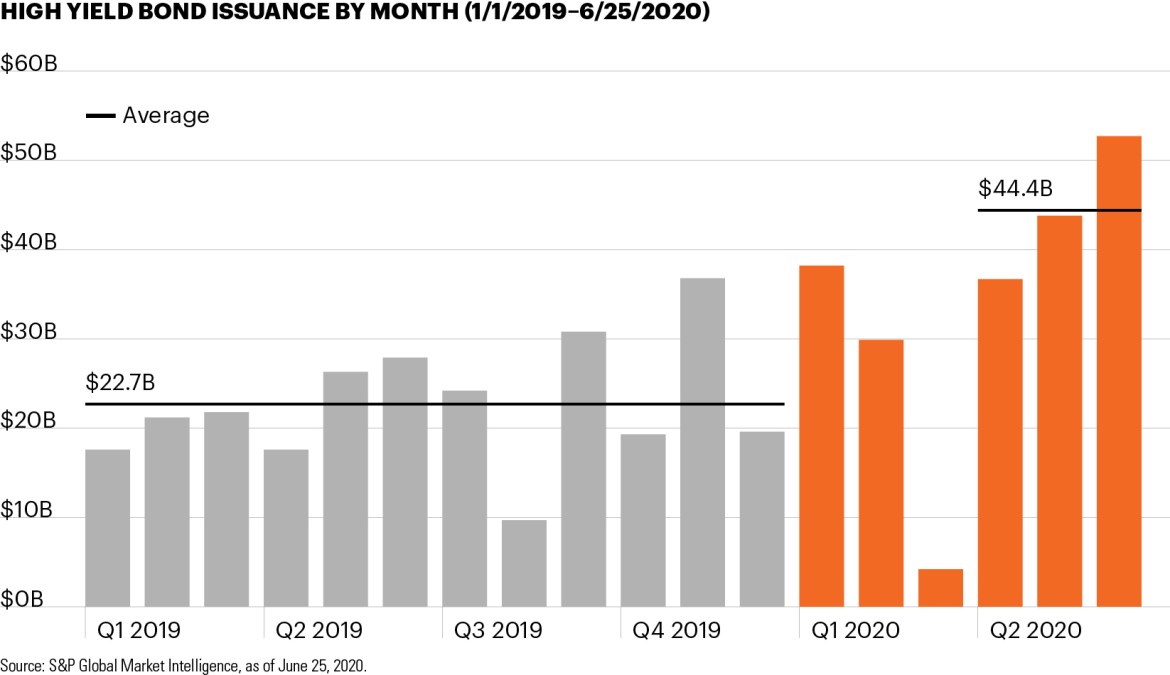

To this end, new high yield bond issuance declined in February and nearly collapsed in March before recovering rapidly – it is now up 40% year over year.1 As the chart highlights, the monthly average of new issuance during the past three months is almost double that of 2019 as corporations (across the investment grade and high yield universes) have raced to issue debt at a faster pace than at any time in well over a decade.1

While massive new issuance has outpaced even record inflows, the Fed’s willingness to intervene directly in corporate bond markets and act as a backstop source of demand has drastically improved sentiment, ultimately lending a constructive outlook for the asset class.

Quarter to date, high yield bonds have returned approximately 10.7%. They are now down just -3.8% YTD and may have room for additional upside.2 Spreads on high yield bonds have declined significantly from their peak but have historically been lower than they are today about 75% of the time.2 In other words, they may have room to fall further. (A bond’s price rises when its spread, or yield above the risk-free rate, declines.)

Despite the broadly supportive picture, many risks remain. Credit fundamentals have weakened amid the pandemic and default rates have risen, leading some market forecasters to think default rates could double by the end of 2020. Against this backdrop, experienced, active management may be more important than ever in discerning which businesses have the strongest balance sheets and operating models or may have been unfairly punished in the broader market sell-off.